The CSRD: what you need to know

Many companies will soon need to start sharing information about their sustainability strategy and impacts. This is set out in the European Commission’s Corporate Sustainability Reporting Directive (CSRD). Are you worried about whether the CSRD applies to you and what you need to do? Find out when to get started, and how.

The CSRD is a key component of the European Green Deal, which aims to enable huge changes in sustainability. With this directive, more consistent and transparent information will become available about how large and listed companies are doing when it comes to sustainability, and what they intend to do about it.

Does the CSRD apply to you?

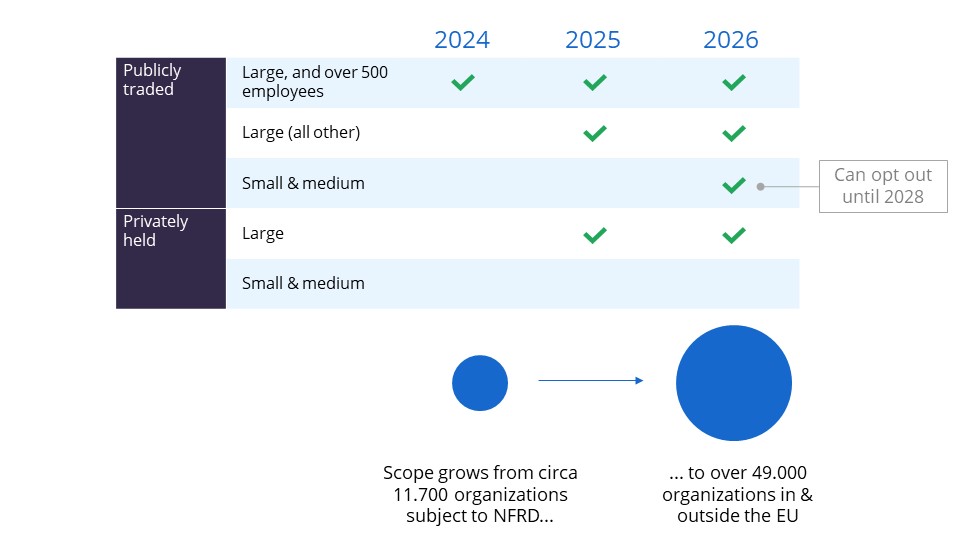

The CSRD was adopted by the European Commission in 2022 and will roll out in waves, from 2024 through 2028. When – and if – your company needs to start complying with the CSRD is determined by your company’s size and whether you’re publicly traded.

The shortest deadline applies to large organizations with over 500 employees that are publicly traded. They’re required to start CSRD compliance in 2024. Other large organizations are to follow in 2025. A company qualifies as ‘large’ in Directive 2013/34/EU Article 3(4) if they meet two of these three criteria:

- Over 250 employees on average in a year

- Over 20.000.000€ total balance sheet

- Over 40.000.000€ net turnover

For many companies, this will be the first time they need to examine their sustainability strategy and reporting structures in detail. Others may have already begun this process as part of the Non Financial Disclosure Regulations (NFRD). Setting up the right sustainability systems – and measuring their impact – will take a significant amount of alignment, resources, and time. However, the benefits of starting the sustainability transformation for your organization are huge.

The CSRD focuses on supporting investor decisions, which most often involves large companies or publicly traded ones on the stock markets. For now, privately held SMEs are outside of the scope of the CSRD. However, this doesn’t mean that SMEs can ignore sustainability or deeper reporting requirements. Sustainability expectations and transparency are growing across society, becoming more important for end consumers, business procurement decisions, and distribution of investment funds needed to grow any business. While it might not be required yet, early investment in sustainability transformation is likely to become part of the foundation for scalable growth for many companies outside the current scope of the CSRD.

What does it take to comply with CSRD?

In general, the CSRD requires companies to disclose their sustainability strategy, impact, and tactics such as targets. To ensure that the information shared is robust, the reports need to be verified by a neutral third-party auditor. This is similar to existing requirements for financial reporting, which have resulted in more robust processes for financial management.

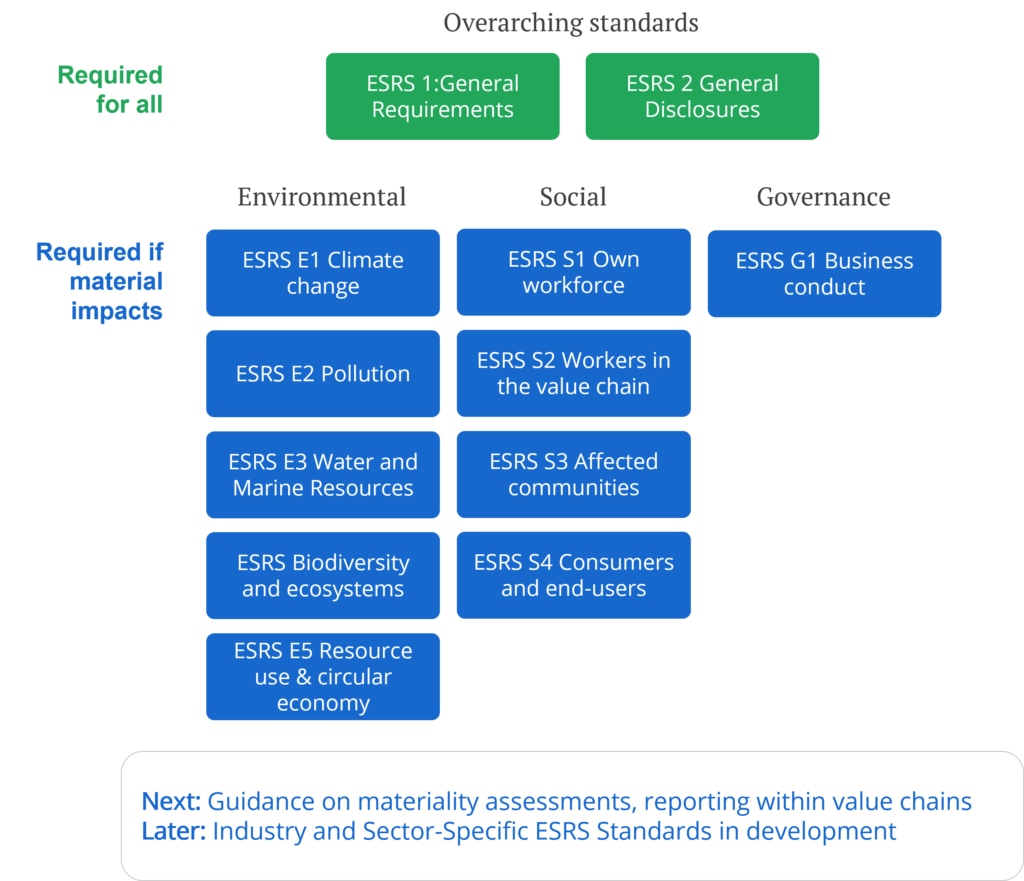

Practically, companies must look to the European Sustainability Reporting Standards (ESRS), published by the European Financial Reporting Advisory Group (EFRAG). The ESRS provides guidance and the required metrics for sharing sustainability information.

The overarching standards ESRS 1 and ESRS 2 are required for all companies subject to the CSRD. These include sharing an overview of the sustainability strategy, risks, opportunities, policies, and targets. This is the minimum reporting obligation that applies to all companies subject to CSRD. The other standards that apply depend on the outcome of your materiality assessment.

Assess where your impacts lie

Companies are required to conduct a materiality assessment, which identifies which environmental, social, and governance issues their business contributes to. For example, a fossil-fuel-based company would find that climate change is a material issue, as fossil fuels release greenhouse gasses that are a key contributor to climate change. The outcome of your company’s materiality assessment determines which additional ESRS standards you must comply with, such as water and marine issues, biodiversity, workers in the value chain, governance, and others. Based on that, you’ll have to measure and report more information, such as climate-based targets, or scope I, II, and III greenhouse gas emissions. It’s also necessary to disclose the methods used for the materiality assessment. A third-party audit helps ensure that the materiality assessment accurately reflects the impacts that a company has.

CSRD is just the beginning of broader sustainability

As of July 31, 2023 the ESRS standards are officially part of the CSRD. However, these standards will continue to evolve. Other standards, such as industry and sector-specific standards, are still in development. Building a future-proof foundation of sustainability management and data will be critical to successfully navigating this dynamic field.

CSRD is an EU-based regulation that will impact international companies beyond EU borders, and is just one of many new changes – and opportunities – arising from the European Green Deal. This regulation will promote an unprecedented level of transparency in sustainability worldwide.

In financial reporting, transparent process control in reporting profits and financial ratios has helped investors make smarter decisions. The CSRD lays the framework for the same to happen in sustainability. As investors and society increasingly realize the value of sustainability for our future, companies will gain a competitive advantage with a strong sustainability strategy and operating model – the same kind of advantage that stable and protected financial profits do today.

The sustainability landscape is constantly evolving. Expectations from customers are changing, regulatory developments are happening in Europe and beyond, and technical advancements are accelerating. Investing in future-proof sustainability now is crucial to helping your organization become future-proof and navigate the complex changes.

Let us help you get started

Would you like some help setting up the metrics and reporting needed for the CSRD? PRé has deep experience with all aspects of sustainability measurements and reporting. We can help you build sustainable competitive advantage for your company, on a robust and transparent foundation.

Ready to do it yourself? Start using SimaPro – the world’s leading software for life cycle assessment for sustainability reporting – to build your data-driven sustainability infrastructure today.

Kimberly Bittler

Database team lead

Kimberly worked at PRé between 2021 and 2023. Initially joining as an Operations Manager, she later moved on to become the Database Team Lead where she helped the newly-created team grow and become a keystone within the company.