A guide to life cycle costing

Life cycle costing is very much similar to the life cycle assessment. In this article, you will find out what are the similarities, types and whether it can be done in SimaPro.

What is life cycle costing (LCC)?

Life cycle costing (LCC) belongs to the group of sustainability tools that focus on flows in connection with the production and consumption of goods and services. They focus on evaluating different flows in relation to various products or services instead of for example regions or nations. LCC is an economic approach that sums up the “total costs of a product, process or activity discounted over its lifetime”. It is associated with all costs occurring from purchase to disposal and can include the costs of externalities (the environmental costs). The idea is that the purchase price often does not reflect the full costs caused by a product over its whole life cycle and hence is not a sufficient indication.

A robust LCC framework will be able to link life cycle assessment (LCA) studies to the monetary cost systems used by business decision-makers. Unless these “dollar-driven” decisions can be assessed in terms of the physical limits of natural systems, it will be difficult to assess progress toward sustainability. Therefore, LCC is seen alongside LCA as two of the three main pillars in an evaluation of sustainability, with the third, social life cycle assessment (s-LCA), which has gained momentum in the last years.

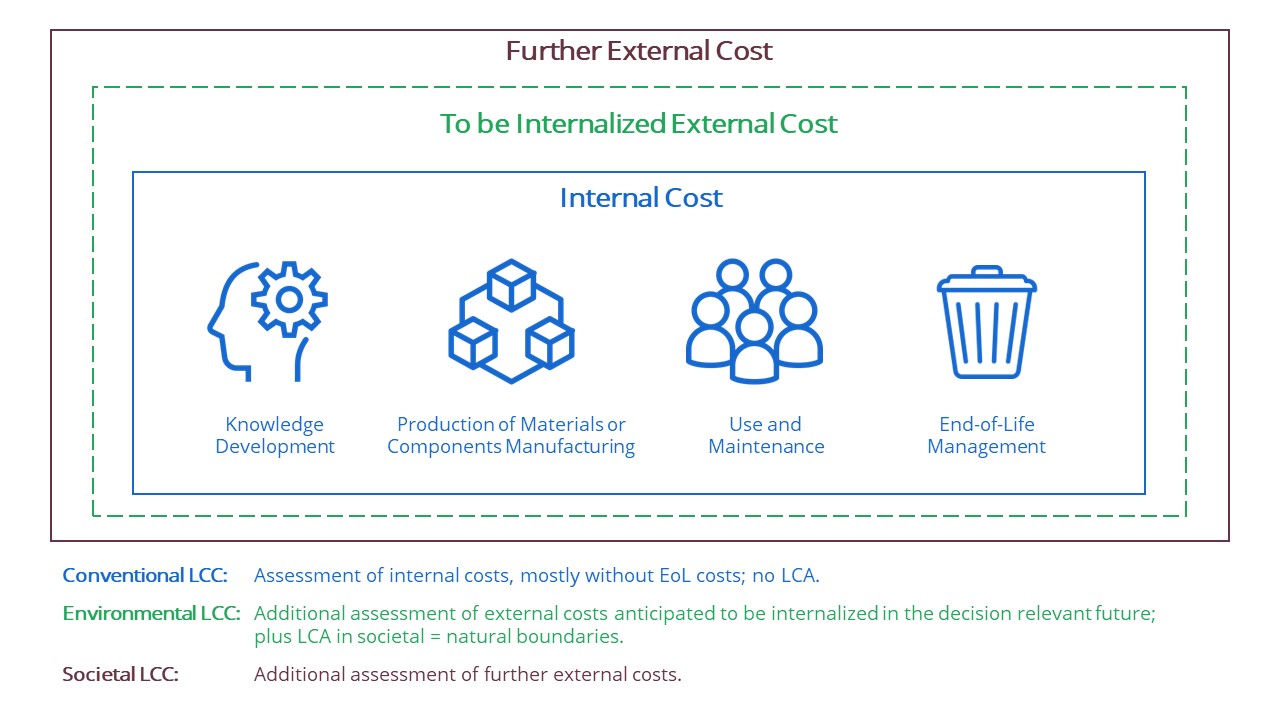

What are the types of life cycle costing?

There are three different types of LCC: conventional, environmental and societal.

- The conventional LCC is, to a large extent, the historic and current practice in many governments and firms, and is based on purely economic evaluation, considering various costs associated with a product that is born directly by a given actor; it is usually determined by the perspective of a single actor, often the product user. In this type of analysis, the external costs are often neglected. LCC is mainly applied as a decision-making tool, to support the acquisition of capital equipment and long-lasting products with high investment.

- Environmental LCC (eLCC) summarizes all costs associated with the life cycle of a product that are directly covered by one, or more, of the actors involved in the product’s life cycle – for example, producers and consumers – including externalities that are anticipated to be internalized in the decision-relevant future. These costs must relate to real money flows. The eLCC is not a stand-alone technique but is seen as a complementary analysis to the environmental life cycle assessment.

- Societal LCC (sLCC) includes monetarization of other externalities, including both environmental impacts and social impacts such as affected social well-being, job quality, etc. This focus makes it a suitable tool for decision-making at the societal level, including governments and policy-makers.

The eLCC as compared to the conventional LCC can be seen as a tool for both external communication and certification as well as labeling, while conventional LCC is more likely to be used as an internal tool. In eLCC, it is obligatory to include all life cycle stages, while the conventional LCC often does not take into consideration the end-of-life costs.

Are there similarities between LCC and LCA?

LCC is very similar to an LCA. Also for LCC, goal and scope (system boundaries, the object of study, allocation, impact assessment), and other aspects need to be defined and aligned with the decisions taken for the LCA in order to obtain an overall consistent analysis.

Basically, an eLCC analysis has a similar structure as an LCA that is conducted in parallel and has the same functional unit and consistency in its scope. The life cycle and system boundaries need to be equivalent, but not necessarily the same as different processes may have different relevance for the environment and for the cost part. For example, research and development will rarely be considered in an LCA, while it is commonly taken into account in LCC. Further, eLCC can be performed from the viewpoint of different “life cycle actors” (as producers, product buyers, or end-of-life actors).

More information about the theory behind LCC can be found in Chapter 15 of the book: Life Cycle Assessment—Theory and Practice.

Since both eLCC and LCA are of a similar structure and can even be interpreted together, it makes sense to conduct both in one software tool such as SimaPro.

Life cycle costing software: SimaPro

Since each organization defines costs differently, and costs are fluctuating almost by definition, no default costs and costing methods are defined in SimaPro. You can define your own “customized” costs and create a related life cycle costing method in SimaPro. To do so, you can follow our accompanying guide.

Emilia Ingemarsdotter

Consultant

Emilia worked at PRé between 2021 and 2024. As a Consultant, she worked on many projects in the fields of LCA, decarbonization, and circular economy – often with a focus on digitalization – and provided PEF trainings.