Navigating the sustainability reporting landscape with LCA

The sustainability reporting landscape is complex and rapidly evolving as climate risks increase, ownership in sustainable transformation grows, and new policies are enacted. Would you like some help successfully navigating this landscape within the EU? Then this article is just for you, with an overview, trends, and explanations. As a champion for life cycle thinking, PRé is involved in finding the links and synergies between life cycle assessment (LCA) and these regulations. We believe LCA is a great tool to help companies comply with regulatory requirements and benefit from the new influx of sustainability data.

Overview of the reporting landscape

The end goal of the sustainability movement is not, of course, that everyone will then finally do sustainability reporting. However, consistent reporting is a critical element of creating the more sustainable future we want – it ensures consistent and fair comparisons that can focus on true progress instead of greenwashing. In addition, measuring the effects you have means you can manage your impact.

However, not all sustainability reporting is the same. In the chart below, you can see a few examples of reporting schemes across the ecosystem. Some reporting schemes are single-issue frameworks, such as the Greenhouse Gas Protocol that focuses only on climate change. Others are broader, such as ISO-certified LCA analyses or analyses using Product Environmental Footprint Category Rules (PEFCR). In the rest of this article, we will discuss reporting standards, voluntary reporting schemes and mandatory reporting requirements.

Standards: how to consistently measure impact

Standards are often the “toolkit” providing technical, actionable guidance needed to consistently measure sustainability metrics. Standards are sometimes incorporated into voluntary and regulatory reporting frameworks as a toolkit for compliance, for example, the European Sustainability Reporting Standards (ESRS) show companies how to comply with the European Union’s Corporate Sustainability Reporting Directive (CSRD). While there are many ongoing efforts to harmonize the various standards and reporting frameworks, not every standard is compatible with every reporting scheme.

PRé Sustainability has helpful guides from our experts that can help you select the right standard for your application, based on our own experience:

Voluntary reporting: being a frontrunner in sustainability

Voluntary sustainability reporting initiatives provide the framework for companies to share sustainability performance data publicly, in a way that makes comparison possible – before they are required to by law or policy. Examples include the Carbon Disclosure Project, which enables organizations to share and manage their environmental impacts, and the Global Reporting Initiative which sets best practices for measuring impacts across subject areas.

Voluntary initiatives provide the opportunity for proactive frontrunners to demonstrate their progress for stakeholders in a transparent and comparable way. These can also help fill in the gaps between different regulatory regimes, some of which may have advanced and comprehensive laws, while others may lag behind, and can help push the state of sustainability regulations across the board to a new level.

Mandatory reporting: the regulatory landscape in the European Union

The regulatory landscape globally is rapidly changing at multiple levels: from international agreements such as the March 2023 agreement to protect biodiversity on the high seas, regional cross-border policies and regulations under the European Green Deal, to initiatives within single countries such as the Inflation Reduction Act of 2022 funding climate action in the United States.

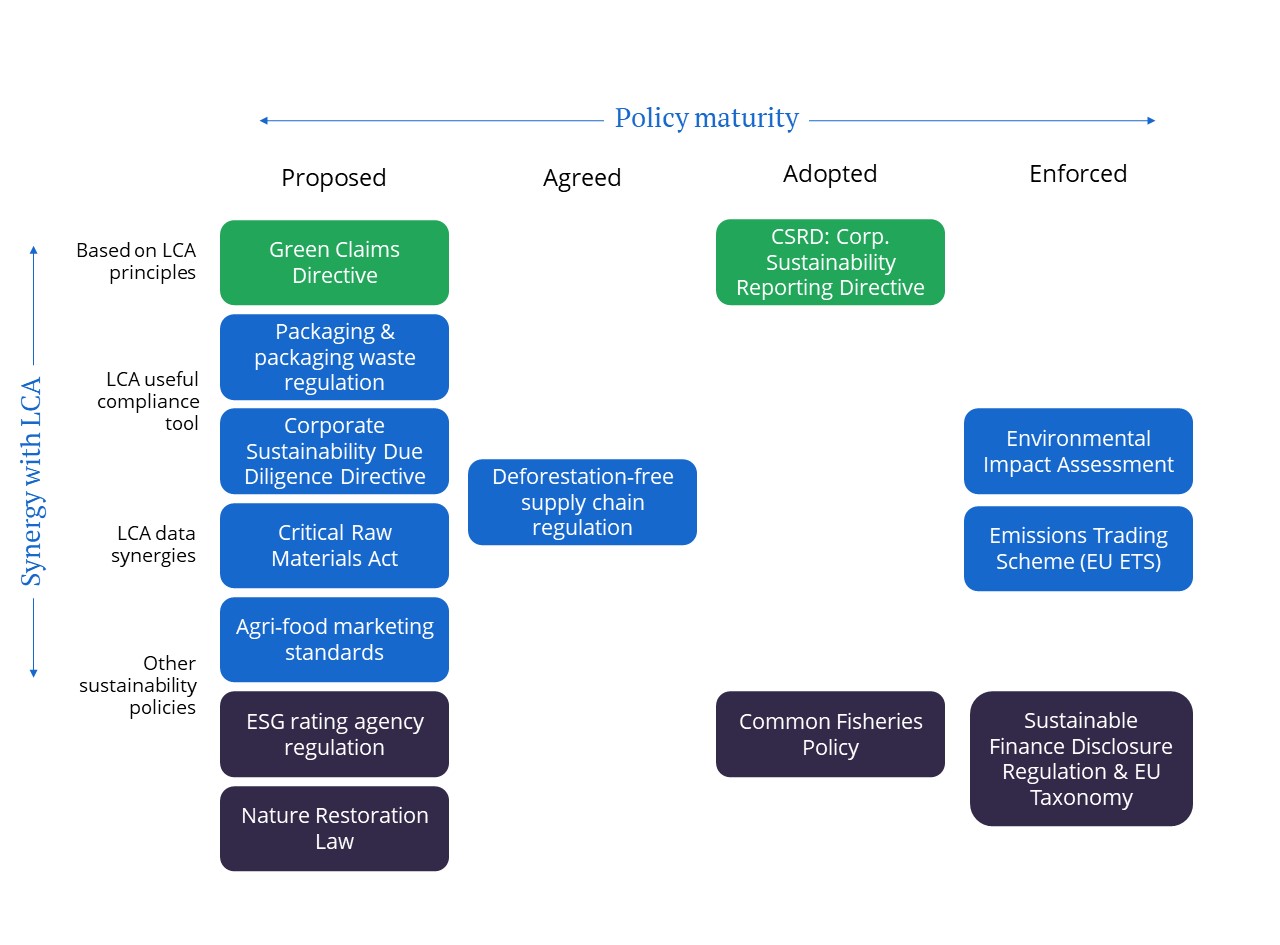

The European Union is a global leader in environmental and sustainability policy and is releasing ground-breaking regulations that further position Europe as a sustainability frontrunner. Policies can come in many forms, from sharing strategic plans, funding opportunities, and creating regulations. Regulations carry mandatory actions that can have a large impact on stakeholders. However, new regulations evolve through a process with stakeholders, maturing from proposed regulations that can be revised with stakeholder engagement, to adopted regulations that have been formally agreed upon.

As policies move through the maturity process, they become increasingly relevant for impacted stakeholders, and require more immediate action. For example, the Green Claims Directive is only in its proposal stage. It may still change depending on political agreement and feedback from stakeholders. In comparison, the Corporate Sustainability Reporting Directive (CSRD) has been formally adopted and will come into force starting in 2024. The CSRD already requires urgent action from the first wave of impacted companies.

Regulations leveraging LCA approaches

Life cycle assessment (LCA) is an important tool for environmental footprinting and especially for compliance with sustainability reporting regulations. There are two key emerging regulations in the EU as of 2023:

- Starting in 2024, the CSRD requires large and listed companies to disclose the link between their strategy and operating models and sustainability in a transparent way. LCA can be helpful to manage environmental data on impacts to comply with the CSRD in an effective way. Read our step-by-step process how.

- The Green Claims Directive has not been finalized as of 2023. This directive aims to simplify and standardize sustainability information to make it easier for consumers to make informed decisions, while reducing the risks of greenwashing. At PRé, we recognize the critical need for this type of standardization as well – it was a key theme arising from talks by scientists and regulators at the 2023 SETAC conference, and we have been involved in LCA harmonization through our work developing Product Environmental Footprint Category Rules (PEFCR).

Regulations with LCA synergies

In addition, many other emerging and mature policies and regulations synergize with LCA. For example:

- The Packaging and Packaging Waste Regulation brings potential new requirements for better packaging design, to enable reuse and set targets for recycled content. As organizations create these new designs, LCA can help contextualize and balance this circularity target with other impact areas. It can also help create an audit trail of implementation across supply chains, and aid decisions and designs with specialized tools such as the Packaging tool or ecodesign.

- The Corporate Sustainability Due Diligence Directive establishes a core duty for large corporations to prevent, identify, and mitigate environmental and human rights impacts in both their own operations and within their value chains. LCA data frameworks are one potential way that directors can track impacts, identify hotspots of risk (e.g. using an approach such as social LCA), and manage their audit and due diligence data in a harmonized approach – even when that extends throughout complex value chains.

- The EU Emissions Trading System (ETS) is a cap-and-trade system creating the first and largest international carbon market, which will control greenhouse gas (GHG) emissions effectively. This requires robust and transparent monitoring of direct GHG emissions, which emission factors within LCA tools like SimaPro can facilitate at scale. LCA captures not just the regulated direct emissions, but can also capture emissions throughout the value chain, creating a cradle-to-grave view of carbon accounting.

- Environmental Impact Assessment (EIA): Since the 1980’s, these directives integrate environmental impacts into the decision-making process for major development projects in both the EU and the USA. These assessments cover a wide range of impact areas, often looking at the “cumulative effect” of “past, present, and reasonably foreseeable” actions. These characteristics are similar to LCA, which may have synergies as a tool to streamline analyses. In addition, EIAs sometimes include a consultation process, gathering feedback from scientists, industry, and the public to inform the decision. These consultations are a rich source of information – one that could help build out the LCA knowledge base more deeply in the future.

Several regulations will require more detail about where products originate. Some laws, such as deforestation-free supply chains, could require this down to the specific site level. This type of geographic specificity can help LCA practitioners make more precise impact assessments, for example by using ecoregions with the Chadhaury et al. 2015 methodology. These initiatives include:

- Deforestation-free supply chains, which requires specific geographic locations of where products were harvested. This can be cross-referenced to satellite-observed land use changes, and helps ensure that products sold in the EU did not cause deforestation.

- The Critical Raw Materials Act will require more detail and assurance about the origins of critical raw materials outside the EU.

- Agri-food marketing standards will require clear origination details on packaging for consumers.

- The Common fisheries policy will require better origination detail for seafood, such as more specific geographical origins that could enable more specific, local impact assessments.

Use LCA frameworks to stay ahead of the curve

The global policy landscape is constantly evolving to better address the critical sustainability challenges our society faces. So are the supporting regional, national, and voluntary regulations and standards that catalyze broader changes. However, key trends are emerging:

- Transparency: Standards and regulations will continue pushing for more transparency across impact areas and industries. Investing in a strong backbone of sustainability reporting systems at a detailed level now can pay dividends later, allowing your business to rise above the crowd as a sustainable leader.

- Harmonization: Many regulations, such as the CSRD, explicitly try to harmonize the approaches between different reporting standards to facilitate truly interoperable data and comparisons across industries. The Green Claims Directive aims to facilitate this explicitly. Across the landscape, we expect that the many standards and large amount of guidance will begin to consolidate under a regulatory framework in the coming years.

- Accountability: Coupled with transparency, legally binding targets such as the Nature Restoration Law and the evolving Emissions Trading Scheme (ETS) provide the accountability to translate ambitions into concrete actions. The CSRD requires audits of information to validate that it is robust and sound, making good comparisons possible. Expect future developments to build more accountability into sustainability reporting, and consider the following question: what could you be doing now to ensure that your processes are robust?

LCA is a robust footprinting approach that spans industries, impact areas, and reporting standards. As we’ve seen, it is often an important tool to help stay compliant with certain regulations, or it can help your company benefit in many ways from the new information that other regulations will help bring about. As an individual company looking towards this future of increasing regulation, one of the best things you can do is invest in a robust, transparent, and detailed data foundation. This will go a long way towards helping your company achieve your sustainability ambitions, and become future-proof in a complex and shifting regulatory environment.

Kimberly Bittler

Database team lead

Kimberly worked at PRé between 2021 and 2023. Initially joining as an Operations Manager, she later moved on to become the Database Team Lead where she helped the newly-created team grow and become a keystone within the company.